Ether (ETH), the digital asset that fuels decentralized applications on the Ethereum network, will be distributed at a consistent yearly linear rate through the block mining mechanism. This rate stands at 0.3 times the total volume of ETH acquired in the pre-sale.

While the most fitting analogy for ETH is “fuel for operating the contract execution engine,” for the purpose of this discussion, we will regard ETH solely as a currency.

There are two prevalent interpretations of “inflation.” The initial pertains to prices, while the latter relates to the total quantity of money in a system – the monetary base or supply. Likewise, this applies to the concept of “deflation.” In this discussion, we will differentiate between “price inflation,” which signifies the escalation of the overall price level of goods and services within an economy, and “monetary inflation,” which refers to the increase in the money supply due to some sort of issuance mechanism. Often, although not always, monetary inflation results in price inflation.

Despite ETH being issued in a predetermined amount annually, the growth rate of the monetary base (monetary inflation) is variable. This rate of monetary inflation diminishes each year, rendering ETH a disinflationary currency (in terms of monetary base). Disinflation represents a specific scenario of inflation where the rate of inflation declines over time.

It is projected that the quantity of ETH lost annually due to transfers to inaccessible addresses is approximately 1% of the monetary base. ETH can be lost due to forgotten private keys, the owner passing away without transmitting the private keys, or intentional destruction by sending to an address that never had a corresponding private key generated.

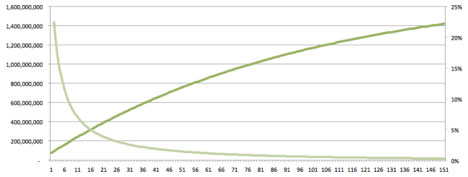

Assuming Ethereum sells 40,000 BTC worth of ETH in the pre-sale, and if the average price is 1500 ETH/BTC, 60,000,000 ETH will be generated in the genesis block and allocated to buyers. Each year, perpetually, 18,000,000 ETH will be issued through the mining process. Taking into account both the generation of new ETH and the loss of existing ETH, in the first year, this represents a monetary inflation rate of 22.4%. In the second year, the rate declines to 18.1%. By the tenth year, the figure drops to 7.0%. In year 38, it reaches 1.9%. And in the 64th year, a level of 1.0% is attained.

{kind=link}

Figure 1. Quantity of ETH in circulation (dark green curve) on the left axis. Monetary base inflation rate (light green curve) on the right axis. Years on the horizontal axis. (Adapted from Arun Mittal with appreciation.)

By around the year 2140, BTC issuance will halt, and since some BTC will presumably be lost each year, the monetary base of Bitcoin is anticipated to begin contracting at that time.

Around the same period, the anticipated rate of annual loss and destruction of ETH will offset the issuance rate. Under this scenario, a quasi-steady state is achieved, and the total supply of existing ETH will no longer expand. If there is still an increasing demand for ETH due to a growing economy, prices will exist in a deflationary environment. This situation does not pose an existential threat for the system, as ETH is theoretically infinitely divisible. Provided the deflation rate is not excessively rapid, pricing mechanisms will adapt, and the system will function smoothly. The traditional primary concern regarding deflationary economies, wage stickiness, is likely to be mitigated since all payment systems will be adaptable. Another common concern, borrowers being compelled to repay loans with a currency that appreciates in purchasing power over time, will also not be an issue if this regime persists, as lending terms will be established to accommodate this.

It is important to note that while monetary inflation remains positive for several years, price levels (tracked as price inflation and deflation) are contingent on supply and demand, thus related to but not solely governed by the issuance rate (supply). Over time, it is expected that the expansion of the Ethereum economy will considerably surpass the growth of the ETH supply, which could result in an appreciation of ETH relative to traditional currencies and BTC.

One of the significant value propositions of Bitcoin was the algorithmically fixed total issuance of the currency, which stipulated that only 21,000,000 BTC would ever be produced. In an era of reckless legacy currency printing in an increasingly futile attempt to mask the excessive debt within the global economic system (accompanied by more debt), the idea of a universally accepted cryptocurrency that can ultimately serve as a relatively stable store of value is appealing. Ethereum acknowledges this and aims to replicate this fundamental value proposition.

Ethereum also acknowledges that a system designed to function as a distributed, consensus-driven application platform for global economic and social frameworks, must place a strong emphasis on inclusivity. One of the numerous strategies we plan to implement to promote inclusiveness is by maintaining an issuance system that embodies some turnover. New entrants into the system will have the opportunity to purchase new ETH or mine for new ETH, regardless of whether they are living in 2015 or 2115. We believe we have achieved a favorable balance between fostering inclusivity and sustaining a stable store of value. Moreover, the consistent issuance, particularly in the early years, will likely render utilizing ETH to establish businesses in the Ethereum economy more profitable than speculative hoarding.