One of the more intriguing long-term practical advantages of the technology and notion behind decentralized autonomous organizations is that DAOs enable us to swiftly prototype and experiment with an element of our social interactions that has arguably lagged behind our swift progressions in information and social technology: organizational governance. While our contemporary communication technology significantly enhances individuals’ naturally limited capacity to both engage and acquire and process information, the governance frameworks we possess today are still reliant on what may now be considered centralized supports and arbitrary categories such as “member,” “employee,” “customer,” and “investor” – characteristics that were arguably initially essential due to the intrinsic challenges of overseeing large groups of individuals up to now, but perhaps are no longer necessary. Presently, it might be feasible to establish systems that are more adaptable and generalized that harness the full power curve of people’s capacity and eagerness to contribute. There exist several new governance frameworks attempting to utilize our innovative tools to enhance transparency and efficacy, including liquid democracy and holacracy; the one I will explore and analyze today is futarchy.

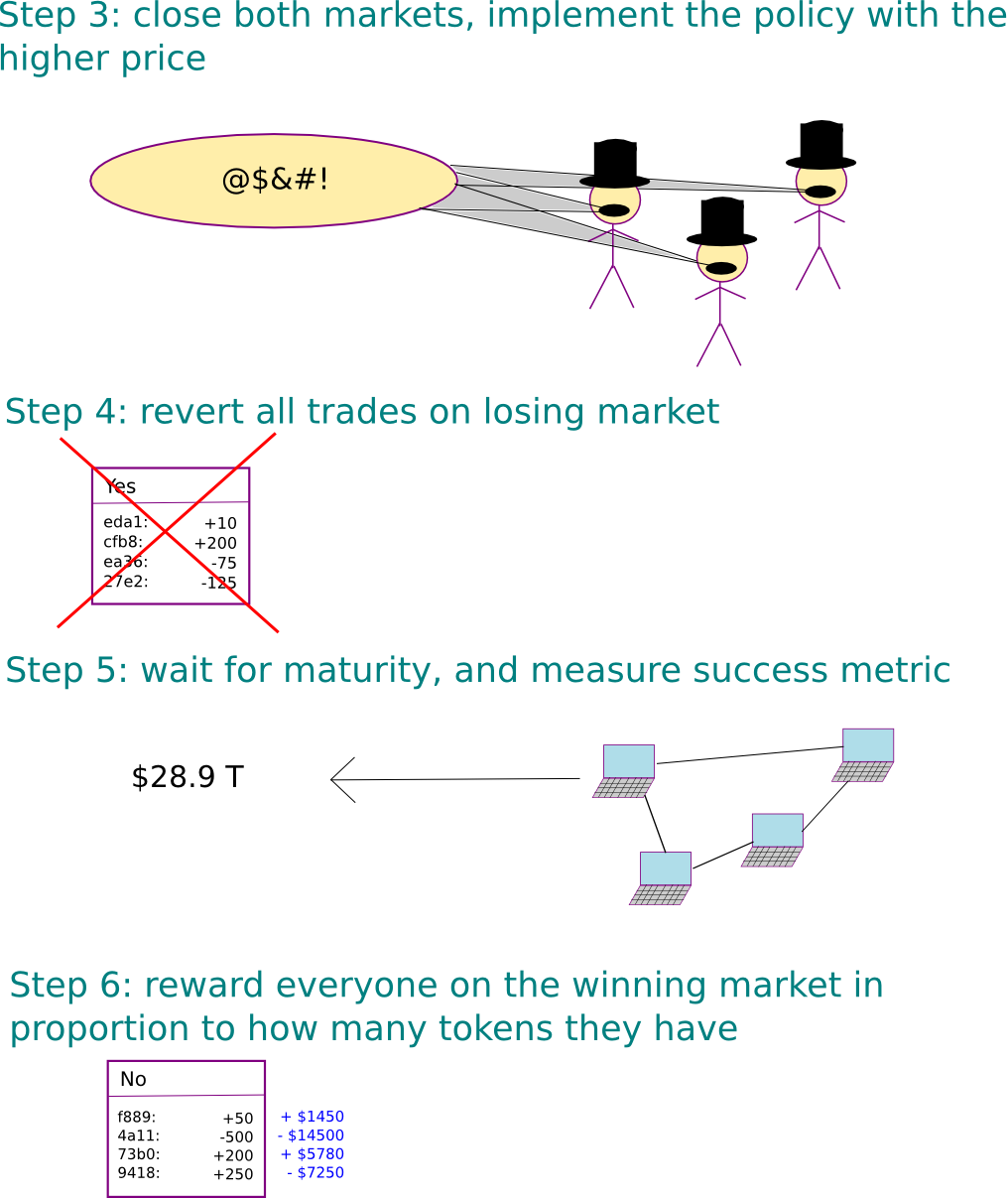

The concept behind futarchy was initially suggested by economist Robin Hanson as a visionary form of governance, encapsulated by the motto: vote values, but wager beliefs. Within this framework, individuals would cast votes not on whether to adopt specific policies, but rather on a metric to assess how effectively their nation (or charity or corporation) is performing, and then prediction markets would be employed to select the policies that optimally enhance the metric. Upon receiving a proposal for approval or disapproval, two prediction markets would be established, each consisting of one asset; one market corresponding to the endorsement of the measure and another to its rejection. If the proposal is accepted, all transactions on the rejection market would be reversed, but in the acceptance market, after a period, everyone holding tokens would be compensated a certain amount based on the selected success metric of the futarchy, and vice versa if the proposal is declined. The market is permitted to operate for some time, and ultimately, the policy with the higher average token price is selected.

Our focus on futarchy, as previously mentioned, is in a slightly varied form and application of futarchy, governing decentralized autonomous organizations and cryptographic protocols; nonetheless, I am illustrating the application of futarchy in a national government first as it is a more recognizable context. To understand how futarchy functions, let’s consider an example.

Imagine that the success metric selected is GDP in trillions of dollars, with a time delay of ten years, and there is a proposed policy: “bail out the banks.” Two assets are issued, each of which guarantees to pay $1 per token per trillion dollars of GDP after a decade. The markets might be allowed to function for two weeks, during which the “yes” token averages a price of $24.94 (indicating that the market believes the GDP after ten years will be $24.94 trillion) while the “no” token averages a price of $26.20. The banks are not bailed out. All transactions on the “yes” market are reversed, and after ten years, everyone holding the asset on the “no” market receives $26.20 each.

Typically, the assets within a futarchy are zero-supply assets, akin to Ripple IOUs or BitAssets. This indicates that the only means by which tokens can be created is through a derivatives market; individuals can place orders to buy or sell tokens, and if two orders align, the tokens are transferred from the buyer to the seller in exchange for USD. It is possible to sell tokens even if you do not possess them; the only stipulation in that case is that the seller must provide some form of collateral to secure the eventual negative payout. An essential implication of the zero-supply characteristic is that, since the positive and negative quantities, and thus rewards offset each other, barring communication and consensus costs, the market is genuinely free to operate.

The Advocacy For

Futarchy has evolved into a contentious topic since the concept was initially proposed. The theoretical advantages are plentiful. Firstly, futarchy addresses the “voter apathy” and “rational irrationality” challenges in democracy, where individuals lack sufficient motivation to even educate themselves about potentially detrimental policies due to the minuscule probability that their vote will influence outcomes (estimated at 1 in 10 million for a US government national election); in futarchy, if you possess or acquire information that others do not, you can significantly profit from it, and if your prediction is incorrect, you incur losses. Essentially, you are effectively betting your money on your beliefs.

Secondly, over time, the market experiences evolutionary pressure to improve; individuals who are ineffective at forecasting policy results will suffer financial losses, and their impact on the market will diminish, whereas those who excel in predicting policy outcomes will see an increase in their capital and their influence on the market. It is noteworthy that this operates in precisely the same manner through which economists argue that traditional capitalism succeeds in optimizing the production of private goods, but in this scenario, it also applies to common and public goods.

Thirdly, it can be posited that futarchy diminishes potentially irrational societal influences on the governance framework. It is a widely recognized truth that, at least during the 20th century, the taller presidential contender has been significantly more probable to secure the election (interestingly, the opposite trend was present prior to 1920; one potential hypothesis is that the switch occurred due to the simultaneous emergence of television), along with the well-known anecdote about voters selecting George Bush because he was the president “they preferred to have a beer with“. In futarchy, the participatory governance framework will likely promote a focus on proposals over personalities, and the main activity is the most introverted and asocial endeavor imaginable: delving into models, statistical evaluations, and trading charts.

A marketplace you would rather share a drink with

The system also gracefully integrates public engagement and expert analysis. Numerous individuals criticize democracy as a slide into mediocrity and demagoguery, favoring decisions to be made by adept technocratic specialists. If it operates effectively, futarchy permits individual experts and even entire analytical firms to conduct their own inquiries and assessments, weave their discoveries into the decision-making by buying and selling on the market, and profit from the disparity in information between themselves and the public – akin to an information-theoretic hydroelectric facility or an osmosis-based power station. However, unlike more rigidly structured and bureaucratic technocracies with a distinct separation between members and non-members, futarchies allow anyone to engage, establish their own analytical firm, and if their analyses succeed, ultimately ascend to the forefront – exactly the type of generalization and adaptability we seek.

The Counterargument

The resistance to futarchy is best encapsulated in two articles, one by Mencius Moldbug and the other by Paul Hewitt. Both articles are extensive, comprising thousands of words, but the general aspects of dissent can be outlined as follows:

- A single dominant individual or coalition desiring a specific outcome can persist in purchasing “yes” tokens on the market and short-selling “no” tokens to manipulate token prices to their advantage.

- Markets, in general, are known to be unstable, and this is largely due to the “self-referential” nature of markets – i.e., they primarily consist of individuals purchasing because they observe others buying, thus they are not effective aggregators of actual information. This phenomenon is particularly hazardous as it can be exploited through market manipulation.

- The estimated effect of a particular policy on a global metric is considerably smaller than the “noise” of uncertainty surrounding what the outcome of the metric will be regardless of the policy enacted, especially in the long run. Consequently, the results from the prediction market could end up being highly uncorrelated with the actual impact that specific policies will have.

- Human values are intricate, and it is challenging to condense them into a single numerical metric; indeed, there may be as many disagreements regarding what the metric should be as there are currently disagreements about policy. Moreover, a harmful entity that in today’s democracy would attempt to lobby for detrimental policy might instead find ways to deceive the futarchy by lobbying for an addition to the metric that is known to correlate highly with that policy.

- A prediction market operates on a zero-sum basis; therefore, with participation inherently incurring non-zero communication costs, it is illogical to engage. As a result, participation may remain quite low, leading to insufficient market depth for experts and analysis firms to derive adequate profit from the information-gathering process.

Regarding the first claim, this video debate featuring Robin Hanson and Mencius Moldbug, with David Friedman (son of Milton) later contributing, serves as an exemplary resource. The argument advanced by Hanson and Friedman is that the existence of an organization successfully performing such activities would foster a market where the prices for “yes” and “no” tokens do not accurately reflect the market’s best knowledge, creating a substantial profit opportunity for those countering the manipulation and thereby driving the price back toward the appropriate equilibrium. To facilitate this, the price used to decide which policy to implement is considered as an average over a specified period rather than at a single moment. As long as the market influence of individuals willing to earn profits by counteracting manipulation exceeds that of the manipulator, the honest participants will prevail and extract a significant amount of funds from the manipulator in the process. Essentially, according to Hanson and Friedman, undermining a futarchy necessitates a 51% attack.

The most prevalent rebuttal to this point, articulated more eloquently by Hewitt, highlights the “self-referential” nature of the markets discussed earlier. If the value for “trillions of US GDP in ten years if we bail out the banks” initiates at $24.94, while “trillions of US GDP in ten years if we do not bail out the banks” starts at $26.20, but eventually the two converge to $27.3 for yes and $25.1 for no, would people truly be aware that the values are distorted and begin trading to adjust,or would they merely perceive the revised prices as an indication of market sentiment and either accept or even strengthen them, as is frequently postulated to occur in speculative bubbles?

Self-reference

There is indeed one reason for optimism in this scenario. Conventional markets may often exhibit self-referential traits, and cryptocurrency markets particularly so due to their lack of intrinsic value (i.e., the only basis for their value is their perceived value), but this self-reference arises partly from reasons beyond merely investors mimicking one another like lemmings. The process is as follows. Imagine a company seeking to generate capital through share issuance, currently possessing a million shares valued at $400, resulting in a market capitalization of $400 million; it is prepared to dilute its shareholders with a 10% increase. Consequently, it can raise $40 million. The company’s market cap is expected to reflect the total dividends it will eventually disburse, with future dividends properly discounted at a specific interest rate; therefore, if the price remains steady, it implies that the market anticipates the company will eventually distribute the equivalent of $400 million in total dividends in present value.

Now, suppose the company’s share price unexpectedly doubles. The company can then raise $80 million, enabling it to undertake twice as many initiatives. Typically, capital investments yield diminishing returns, but this isn’t always the case; it could occur that with the additional $40 million in capital, the company might generate double the profit, thus justifying the new share price – even if the spike from $400 to $800 was caused by manipulation or random fluctuations. Bitcoin exhibits this phenomenon in a particularly distinct manner; as the price rises, all Bitcoin users experience increased wealth, allowing them to establish more ventures, which rationalizes the elevated price level. The absence of intrinsic value in Bitcoin means that the self-referential effect is the sole factor influencing its price.

Prediction markets lack this characteristic altogether. Beyond the prediction market itself, there exists no credible mechanism by which the price of the “yes” token on a prediction market will impact the GDP of the US a decade from now. Thus, the only means by which self-reference could occur is through the “everyone follows everyone else’s judgment” phenomenon. However, the magnitude of this effect is open to discussion; perhaps due to the very acknowledgment of its existence, a culture of astute contrarianism has developed in investments, and politics is certainly a domain where individuals are inclined to uphold unconventional perspectives. Furthermore, in a futarchy, the relevant aspect is not how elevated individual prices are, but which one of the two is higher; if you are convinced that bailouts are detrimental, but notice that the yes-bailout price is currently $2.2 higher for some unknown reason, you realize that something is amiss so, theoretically, you might be able to reliably profit from that.

Absolutes and differentials

Herein lies the essence of the true issue: it is unclear how one could do so. Consider a more extreme scenario than the yes/no bailouts decision: a company employing a futarchy to ascertain how much to compensate their CEO. There have been studies indicating that ultra-high-salary CEOs often do not enhance company performance – in fact, quite the opposite. To address this dilemma, why not leverage the power of futarchy to determine what value the CEO genuinely contributes? Establish a prediction market for the company’s performance should the CEO remain, and should the CEO depart, and set the CEO’s salary as a standard percentage of the differential. This approach can also be extended to lower-tier executives and, if futarchy proves to be remarkably effective, even to the most junior employee.

Now, imagine that you, as an analyst, estimate that a firm utilizing such a framework will have a share price of $7.20 in a year if the CEO remains, with a 95% confidence interval of $2.50 (i.e., you’re 95% confident the price will be between $4.70 and $9.70). You also estimate that the CEO’s contribution to the share price is $0.08; the 95% confidence interval you possess here ranges from $0.03 to $0.13. This is quite realistic; generally, errors in variable measurement are proportional to the value of that variable, hence the variation regarding the CEO will be much narrower. Now suppose the prediction market has the token priced at $7.70 if the CEO continues in their role and $7.40 if they exit; in summary, the market perceives the CEO as exceptional, whereas you hold a different view. But how can you benefit from this?

The instinctive response would be to purchase “no” shares and short-sell “yes” shares. But how many of each? You might assume “the same quantity of each, to balance the equation,” but the issue is that the probability of the CEO retaining their position is significantly above 50%. Consequently, the “no” trades will likely be reversed while the “yes” trades won’t, meaning that alongside shorting the CEO, you’re also assuming a substantially greater risk by shorting the company. If you were aware of the percentage change, you could equilibrate the short and long purchases such that, net, your exposure to unrelated volatility is null; however, since you don’t, the risk-to-reward ratio becomes exceedingly high (and even if you did know, you would still face the company’s aggregate volatility; you just wouldn’t be skewed in any particular direction).

From this, we can deduce that futarchy is likely more effective for large-scale decisions, but significantly less so for nuanced tasks. Thus, a hybrid framework may be more beneficial, whereby a futarchy selects a political party every few months, and that party then makes decisions. This may sound like conferring absolute control to one party, but it is not; note that if the market harbors concerns regarding single-party dominance, parties could voluntarily organize themselves into coalitions of diverse factions with competing ideologies, which the market would prefer; in fact, we could implement a system where politicians register as individuals and anyone from the public can propose a combination of politicians for election to parliament, with the market reaching a conclusion about all combinations (although this would still have the drawback of being more personality-driven).

Futarchy and Protocols and DAOs

The aforementioned discussion primarily addressed futarchy as a political framework for governing institutions, and to a lesser degree corporations and nonprofits. In governance, when we apply futarchy to specific laws, particularly those with relatively minor effects like “cut the patent duration from 20 years to 18 years,” we encounter many of the challenges previously highlighted. Additionally, the fourth argument against futarchy mentioned earlier, thecomplexity of values remains a notable concern, as outlined previously, a significant fraction of political discord revolves around what the accurate values should be. Considering these apprehensions, along with the overall sluggishness of political systems, it appears improbable that futarchy will be adopted on a national level in the near future. In fact, it has yet to truly be tested at the corporate level. Now, though, a completely new category of organizations exists for which futarchy may be far more compatible and where it might truly flourish: DAOs.

To explore how futarchy for DAOs could function, let’s describe a potential protocol that could operate on the Ethereum platform:

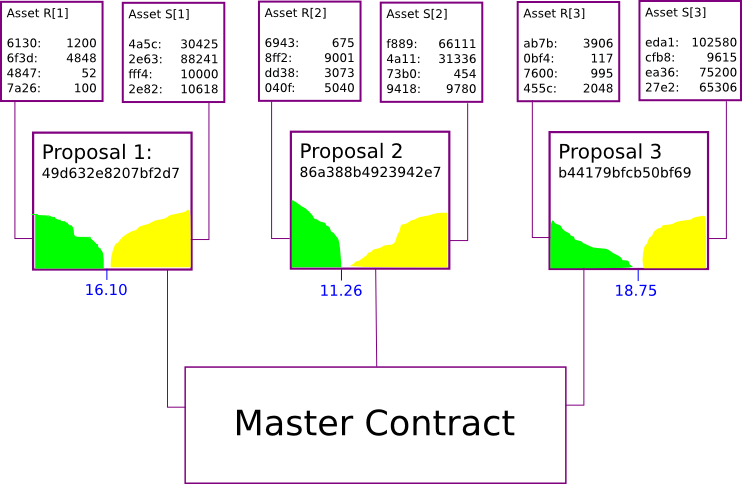

- In each cycle, T new DAO-tokens are generated. At the beginning of a cycle, anyone can propose how those tokens should be allocated. To simplify, we can state that a “proposal” merely consists of “send funds to this address”; the specific plan for how those funds will be utilized would be conveyed through some higher-level channel like a forum, and trustless proposals could be executed through a smart contract. Let’s assume that n such proposals, P[1] … P[n], are submitted.

- The DAO creates n pairs of assets, R[i] and S[i], and distributes the T units of each token type in a random manner (e.g., to miners, to DAO token holders, based on a formula determined through previous futarchies, etc.). The DAO also establishes n markets, with market M[i] facilitating trades between R[i] and S[i].

- The DAO monitors the average price of S[i] quoted in terms of R[i] across all markets, allowing the markets to operate for b blocks ( for example, 2 weeks). When the period concludes, if market M[k] shows the highest average price, then policy P[k] is selected, and the next cycle commences.

- At this stage, tokens R[j] and S[j] for j != k become worthless. Token R[k] has a value of m units of some external reference asset (for example, ETH in a futarchy on the Ethereum network), while token S[k] is valued at z DAO tokens, where a reasonable figure for z might be 0.1, and m adjusts to maintain sensible spending. It’s important to note that for this mechanism to function, the DAO would also need to sell its own tokens for the external reference asset, demanding a separate allocation; possibly, m should be aimed for so that the token spending required to acquire the necessary ether is zT.

Essentially, this protocol is executing a futarchy that aims to enhance the token’s value. Now, let’s examine some distinctions between this type of futarchy and futarchy-for-government.

To begin with, the futarchy here makes only a very specific type of decision: to whom to allocate the T tokens generated in each round. This factor alone renders the futarchy here considerably “safer”. A futarchy-as-government, especially if unregulated, carries the possibility of encountering severe unforeseen complications when tied to the fragility-of-value dilemma: imagine we agree that GDP per capita, potentially with inclusions for health and environmental factors, is the best value function to adopt. In such a scenario, a policy that eliminates 99.9% of the population who aren’t wealthy would prevail. If we select straightforward GDP, a policy might succeed that heavily subsidizes those relocating their businesses and residences to the country, possibly employing a 99% one-time capital tax to finance the subsidy. Of course, in practice, futarchies would refine the value function and draft a new bill to negate the original legislation prior to enacting any egregiously obvious situations, but if such reversals happen too often, then the futarchy essentially deteriorates into a conventional democracy. Here, the worst outcome would be for all the N tokens in a given round to be awarded to someone who squanders them.

Secondly, note the different approach regarding the functioning of the markets. In traditional futarchy, we possess a zero-total-supply asset that appears through derivatives market trading, and trades on the failing markets are reverted. Conversely, here we release positive-supply assets, and the means by which trades are reversed is that the entire issuance process is essentially rolled back; both assets on all unsuccessful markets become worthless.

The most significant distinction here is whether individuals will engage in participation. Let’s revisit the earlier critique of futarchy, that it is illogical to join since it constitutes a zero-sum game. This creates somewhat of a paradox. If you have certain insider knowledge, you might perceive it as rational to partake since you possess information others lack, altering your expectations about the eventual settlement price of the assets compared to the market’s; thus, you should profit from the discrepancy. Conversely, if everyone adopts this reasoning, even some individuals with insider information might end up at a loss; therefore, the valid criterion for participation resembles “you should engage if you believe you possess superior insider information compared to other participants”. However, if everyone believes this, the equilibrium will shift to no one engaging.

In this scenario, the dynamics differ. Individuals engage by default, and it proves more challenging to define what non-participation entails. You could convert your R[i] and S[i] tokens for DAO tokens, but if there is a motivation to do so, it may indicate that R[i] and S[i] are undervalued, creating an incentive to acquire both. Moreover, holding only R[i] does not signify inactivity; instead, it reflects a bearish sentiment.on the advantages of policy P[i]; similarly with holding solely S[i]. Indeed, the nearest concept to a “default” strategy is maintaining whatever R[i] and S[i] you obtain; we can model this prediction market as a zero-supply market alongside this additional initial allocation, which renders the “just hold” method as a default. Nonetheless, it can be argued that the threshold for participation is considerably reduced, leading to increased involvement.

It’s also essential to observe that the optimization goal is more straightforward; the futarchy does not aim to regulate the rules of an entire government, but instead focuses on enhancing the value of its own token through budgetary allocation. Identifying more intriguing optimization objectives, possibly those that penalize common detrimental actions taken by existing corporate entities, remains an unresolved challenge yet a critical one; at that point, the issues of measurement and metric manipulation may once again gain prominence. Finally, the actual daily governance of the futarchy adheres to a hybrid model; disbursements are conducted once per epoch, yet the management of funds within that timeframe can be entrusted to individuals, centralized bodies, blockchain entities, or potentially other DAOs. Therefore, we can anticipate significant differences in expected token value among the proposals, asserting that the futarchy will indeed be quite effective—at least more efficient than the current favored method of “five developers decide”.

Why?

What are the tangible advantages of implementing such a framework? What issues arise from merely having blockchain-based organizations that adhere to more conventional governance structures, or even more democratic alternatives? Given that most readers of this blog are already proponents of cryptocurrency, we can succinctly state that the underlying reason for this is analogous to our preference for utilizing cryptographic protocols over centrally governed systems—cryptographic protocols necessitate much less reliance on central authorities (if you are not predisposed to doubt central authorities, the argument can be reformulated as “cryptographic protocols can more readily adapt to achieve the efficiency, equity, and informational benefits of being more participative and inclusive without necessitating trust in unknown parties”). Regarding social consequences, this simplified version of futarchy is far from perfect, as it still resembles a profit-maximizing corporation; nevertheless, the two significant enhancements it offers are (1) making it more difficult for executives managing the funds to deceive both the organization and society for their short-term gains, and (2) establishing governance that is radically open and transparent.

However, up until now, one prominent pain point for a cryptographic protocol has been how that protocol can finance and govern itself; the primary workaround, a centralized organization with a one-time token launch and presale, is essentially a workaround that generates initial funding and initial governance at the expense of initial centralization. Token sales, including our own Ethereum ether sale, have sparked debates, largely due to how they introduce this flaw of centralization into what is otherwise a purely decentralized cryptosystem; however, if a novel protocol begins by establishing itself as a futarchy from the very start, then that protocol can accomplish incentivization without centralization—one of the key breakthroughs in economics that render the cryptocurrency sector generally worth observing.

Some may contend that inflationary token systems are undesirable and that dilution is detrimental; however, a crucial point is that if futarchy operates effectively, this model is assured to be at least as efficient as a fixed-supply currency, and in scenarios involving a nonzero amount of potentially fulfillable public goods, it will be unequivocally superior. The reasoning is straightforward: it’s always feasible to devise a proposal that channels the funds to an unspendable address, thus any proposal that prevails would need to outperform that baseline as well.

So what are the initial protocols that we anticipate seeing employing futarchy? In theory, any of the higher-level protocols that have their own cryptocurrency (e.g., SWARM, StorJ, Maidsafe) but lack their own blockchain could gain advantages from implementing futarchy atop Ethereum. All they would require is to execute the futarchy in code (something I have commenced doing already), create an appealing user interface for the markets, and launch it. Although technically every futarchy that initiates will be identical, futarchy is Schelling-point-dependent; if you establish a website surrounding one specific futarchy, label it “decentralized insurance,” and cultivate a community around that concept, it is more likely that this particular futarchy will succeed if it genuinely fulfills the promise of decentralized insurance, leading the market to favor proposals that are directly related to that development path.

If you’re creating a protocol that will include a blockchain but doesn’t yet exist, you can utilize futarchy to oversee a “protoshare” that will eventually transition over; and if you are developing a protocol with a blockchain from the outset, you can always embed futarchy straight into the core blockchain code itself; the only modification will be the need to identify an alternative to the “reference asset” usage (e.g., 264 hashes might function as a trustless economic unit of account). Naturally, even in this form, futarchy cannot guarantee success; it remains an experiment and may indeed prove less effective than other systems like liquid democracy—or perhaps hybrid solutions will be optimal. Ultimately, experiments are at the heart of the cryptocurrency endeavor.